HOP PHU MANUFACTURING AND TRADING JSC.,

August 10, 2021News

August 29, 2021

Being a major importer of ethylene, China will be adding eight ethylene crackers in 2021, with a total capacity of 7.8 million tons. This will raise China’s ethylene capacity to around 40 million tons by end 2021.

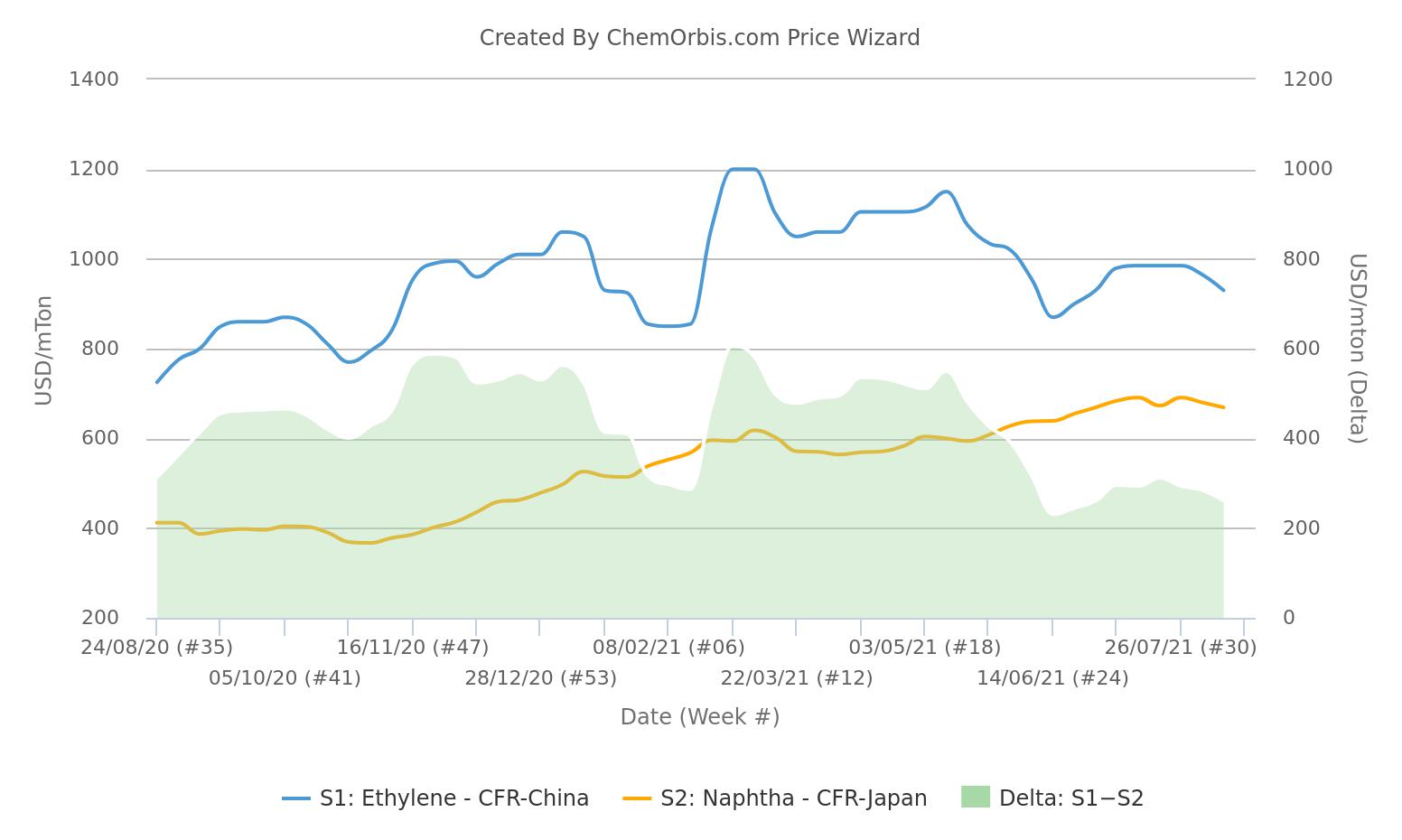

The key CFR NEA ethylene spread to benchmark CFR Japan naphtha was assessed at $261/ton on August 16, just above the typical break-even of $250/ton for integrated producers, according to ChemOrbis Price Wizard.

“Asian naphtha-fed steam cracker operators would likely consider reducing their operating rates as margins for key olefins are now razor-thin, and may fall to a negative territory,” a Western trader noted.

Spot ethylene prices were assessed at $950/ton CFR China and $920/ton CFR Southeast Asia on August 16, down $15/ton on the week.

South Korea’s LG Chemical and KPIC cut cracker run rates

In fact, South Korea’s LG Chemical and KPIC have reportedly cut cracker run rates as current production economics do not justify running these facilities at full capacity.

“As the margin between naphtha and ethylene narrows significantly, or gets into negative territory, it is more economical to purchase ethylene from the spot market rather than produce by ourselves, given the higher crude and naphtha prices,” said an Asia-based producer.

South Korea’s LG Chemical produces some 3 million tons/year of ethylene. The company has a cracker located in Yeosu with 1.16 million tons/year of ethylene, and another 1 million tons/year ethylene cracker located in Daesan. Its third and newest facility in Yeosu produces 800,000 tons/year ethylene and 400,000 tons/year propylene. The plant was started up in early June this year. The producer had announced earlier that run rates had been cut by 10%, to 90% but the current production rate is reportedly at 80%.

Additionally, Korea Petrochemical Industry Co (KPIC) has also reportedly cut production at its Onsan facility, which produces 800,000 tons/year of ethylene and 410,000 tons/year of propylene. It is unclear what the current run rate at the Onsan cracker is.

Reduced demand for naphtha

While the new cracker start-ups in South Korea and China have boosted overall demand for naphtha, the narrowing ethylene margin would lead some crackers to reduce run rates, which will cap demand for cracker-feed naphtha.

The Asian naphtha market was long and pricing had been competitive, but earlier crude price gains had driven naphtha prices higher, with gains of $67/ton seen since March 15, according to price data from ChemOrbis Price Wizard.

Ethylene to CFR China PE, MEG, SM spread at negative

Sentiment has been tempered by uncertainty over downstream markets’ recovery.

Exacerbating the slow demand recovery is Asia and China’s renewed surge in delta variant related Covid-19 infections and lockdowns across major cities in China, Japan, Taiwan, Southeast Asia, and India. Demand recovery has slowed as manufacturing/factory production stalls or gets reduced, and trading activities are also crimped.

The weakness of downstream markets and the lack of pricing support is evident from downstream PE, MEG, and SM prices. PE prices had held steady until last week, when prices fell on weak demand. With HDPE/LLDPE at $1080-1200/ton CFR China/SEA, it is at negative margin for China PE producers, and still above positive margin for Southeast Asia PE producers.

“For MEG, at $665-670/ton CFR China, it is at a negative margin with ethylene at $950/ton CFR China. For SM, at $1160-1170/ton CFR China, and with benzene at around $970/ton, it is also at a negative margin,” said a trader.

Collected by: Daniel

{kind=link}

{kind=link}

{kind=link}